What Is a Drop Line Overdraft (DLOD)?

A Drop Line Overdraft is a credit limit offered for a specific tenure, where the available limit reduces (or “drops”) every month or quarter as you repay.

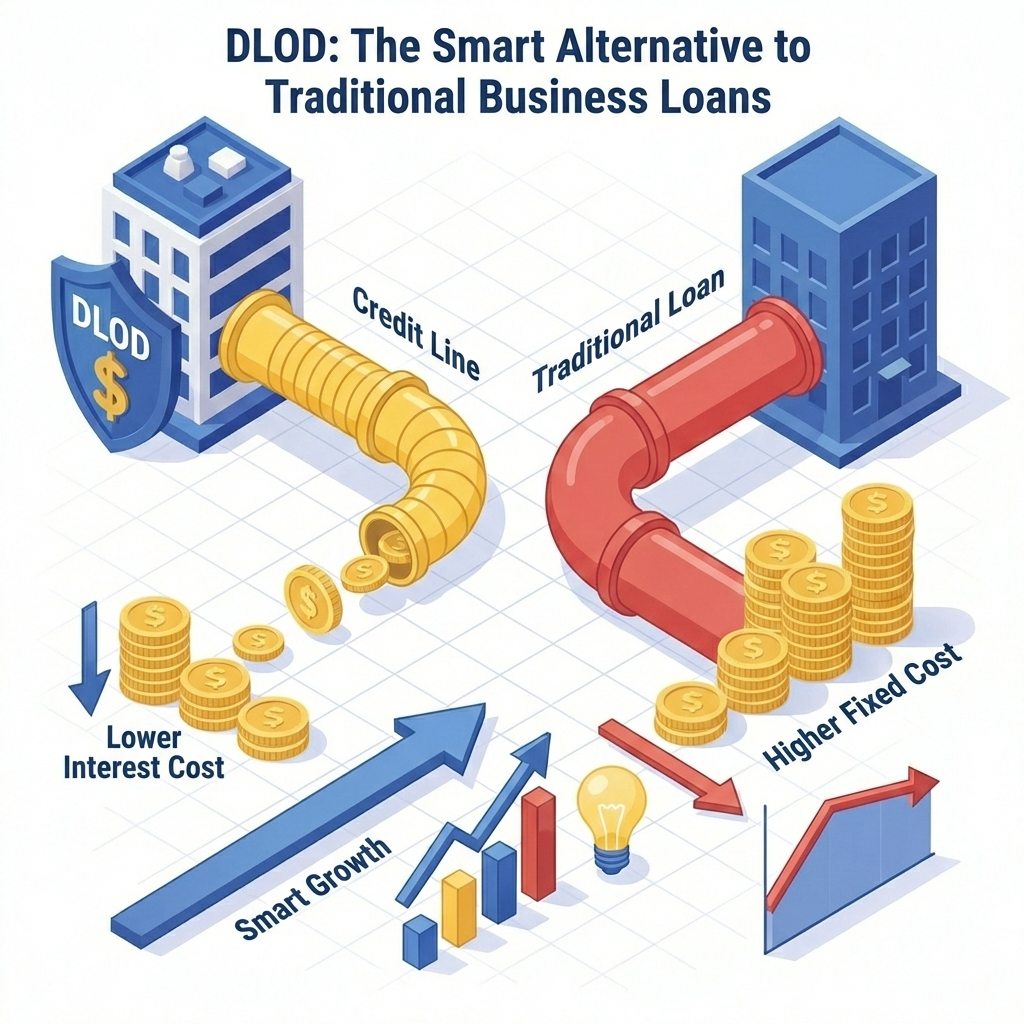

Unlike a term loan where you pay EMIs on the full amount, in a DLOD you pay interest only on the amount you actually use — making it a smarter, cheaper financing option.

Top Benefits of a Drop Line Overdraft

1. Interest on Usage, Not Limit

You pay interest only on the funds utilized, not on the entire limit. That means you save more every month.

2. Flexible Withdrawals and Repayments

No fixed EMI pressure — withdraw when you need funds and repay as per your business inflow.

3. Cost-Effective for Working Capital

DLOD is perfect for managing operational costs, vendor payments, or seasonal cash flow gaps.

DLODOverdraftBusiness Finance

Subscribe to Newsletter

Get the latest financial tips and insights delivered to your inbox